The Angio Suites Market encompasses integrated interventional radiology systems designed to facilitate minimally invasive diagnostic and therapeutic procedures for cardiovascular, neurovascular, and peripheral vascular conditions. These advanced suites combine high-resolution imaging modalities—such as flat-panel detectors, 3D rotational angiography, and real-time fluoroscopy—with patient monitoring and navigation tools. Clinicians benefit from enhanced visibility, reduced radiation exposure, and improved procedural efficiency, which together drive better patient outcomes and shorter hospital stays.

The need for Angio Suites Market is underscored by rising incidences of stroke, coronary artery disease, and peripheral artery disease, along with the growing preference for image-guided interventions over traditional open surgeries. In addition, hospital administrators prioritize solutions that optimize workflow and offer robust market insights into equipment utilization and maintenance. As healthcare systems worldwide seek to control costs and improve clinical efficacy, Angio Suites stand out for their ability to integrate seamlessly with electronic health records and support advanced software analytics.

The angio suites market is estimated to be valued at USD 2.18 Bn in 2025 and is expected to reach USD 3.28 Bn by 2032, growing at a compound annual growth rate (CAGR) of 6.00% from 2025 to 2032.

Key Takeaways

Key players operating in the Angio Suites Market are:

-Siemens

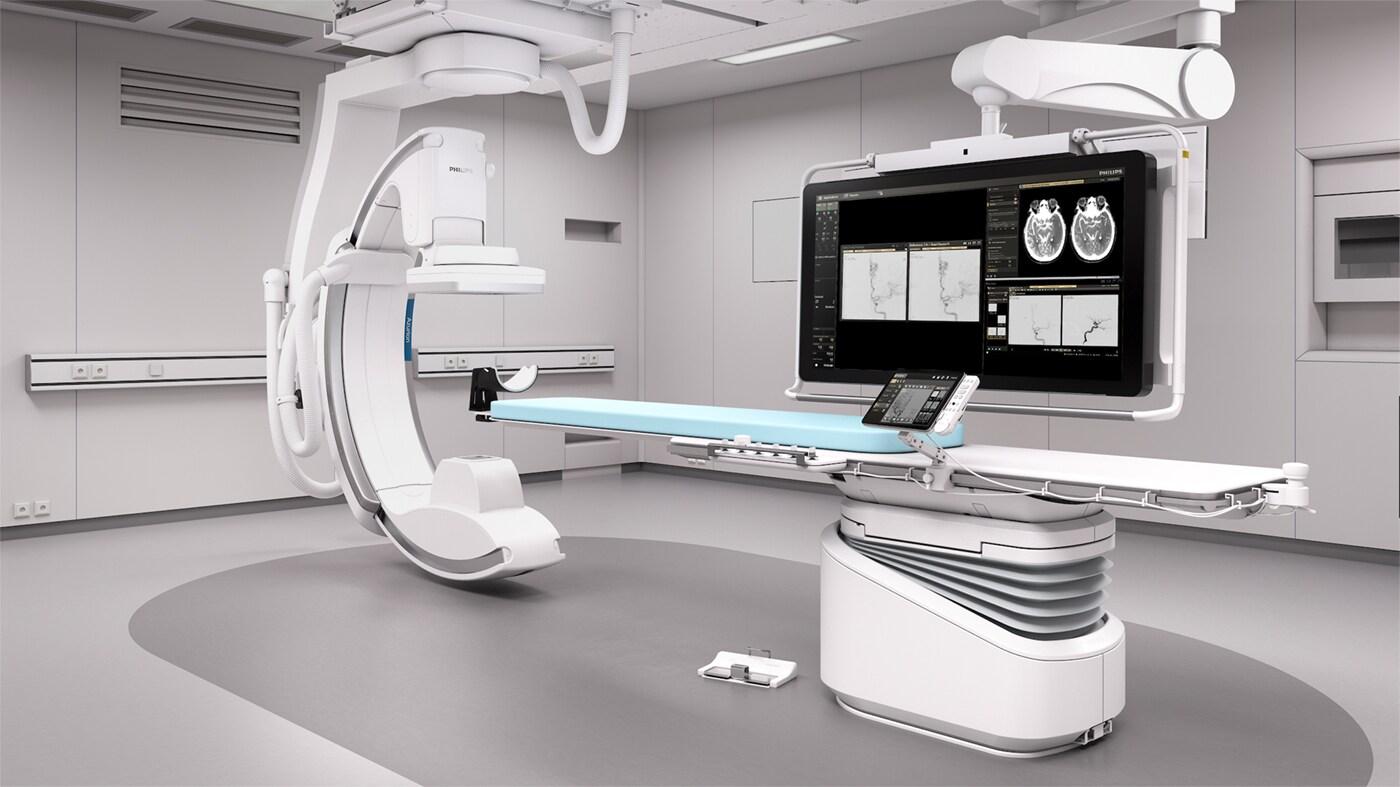

-Koninklijke Philips N.V.

-Hitachi, Ltd.

-General Electric

-Shimadzu Corporation

These market companies continuously invest in R&D to launch next-generation suites that address evolving market trends, enhance image clarity, and streamline interventional workflows. By forging strategic partnerships and leveraging global service networks, they aim to capture greater market share and strengthen their industry position.

The Angio Suites Market presents significant market opportunities driven by growing demand for minimally invasive procedures, integration of artificial intelligence for predictive analytics, and the expansion of hybrid operating rooms. Emerging economies in Asia Pacific and Latin America offer untapped potential as healthcare infrastructure improves. Additionally, the shift toward value-based care models creates openings for providers to adopt suites that deliver comprehensive market research insights on procedure volume, equipment utilization, and patient outcomes, thus supporting business growth strategies.

Global expansion of the Angio Suites Market is propelled by North America’s strong healthcare expenditure and favorable reimbursement policies, followed by Europe’s emphasis on interventional cardiology. Asia Pacific is set to witness rapid growth due to increasing industry size, rising geriatric population, and government initiatives to bolster public healthcare. Latin America and Middle East regions are gaining momentum as market players establish local service centers and leverage distributor partnerships to overcome market challenges, optimize supply chains, and ensure timely after-sales support.

Market drivers

Technological advancements represent a primary market driver for the Angio Suites Market, reshaping the market dynamics and driving market growth. Innovations such as hybrid imaging platforms, AI-powered analytics, and real-time 3D visualization enable clinicians to perform complex interventions with greater precision and reduced procedure time. Upgraded flat-panel detectors and advanced C-arms deliver superior image quality at lower radiation doses, addressing market restraints related to patient and operator safety. In addition, software enhancements offer predictive maintenance features that minimize downtime and operational costs. These technological improvements not only support efficient workflow integration but also open new market segments—such as peripheral interventions and stroke management—by providing comprehensive market insights and robust performance metrics. As a result, ongoing R&D efforts continue to accelerate adoption rates, bolster market forecast projections, and create a favorable environment for sustained business growth.

PEST Analysis

Political: The Angio Suites Market is heavily influenced by evolving healthcare regulations and reimbursement frameworks implemented by governments worldwide, with policymakers prioritizing minimally invasive diagnostic and interventional procedures that drive the adoption of advanced imaging infrastructure; public funding initiatives, standardization of quality metrics, stringent regulatory audits, and cross-border trade agreements further shape national procurement policies, trade tariffs, and supply chain resilience, obliging manufacturers to navigate complex approval pathways and local content requirements.

Economic: The broader economic environment, characterized by fluctuating government healthcare budgets, shifts in gross domestic product growth rates, variable hospital investment cycles, and inflationary pressures in equipment manufacturing costs, directly affects capital expenditure decisions on angio suites; evolving insurance reimbursement schemes, disparities in private versus public hospital funding, and a growing emphasis on cost-effectiveness assessments and long-term value propositions guide decision-making processes and influence market growth trajectories.

Social: Demographic shifts, notably aging populations and increased prevalence of chronic cardiovascular conditions, underpin expanding clinical adoption of angio suites, while heightened patient awareness of minimally invasive treatments, rising healthcare literacy, patient preference for outpatient procedures, and broader urbanization trends drive demand; moreover, the integration of telemedicine and remote patient monitoring capabilities, coupled with growing emphasis on procedural efficiency and reduced hospital stays, further accelerate acceptance across diverse socioeconomic demographics.

Technological: Rapid advancements in high-resolution imaging technologies, including flat-panel detectors, three-dimensional rotational angiography, and hybrid imaging fusion capabilities, are driving product differentiation and elevating clinical outcomes by enabling precise visualization of vascular anatomy and interventional guidance, thereby enhancing procedural accuracy and reducing radiation exposure. Moreover, the integration of artificial intelligence algorithms for image reconstruction, real-time decision support, workflow automation, and cloud-based connectivity platforms to facilitate remote diagnostics and interoperability with electronic health records is accelerating innovation cycles and reshaping competitive dynamics in the market.

Regional Value Concentration

North America commands the largest market share in terms of value adoption for angio suites, owing to its advanced healthcare infrastructure, high procedural volumes, and established reimbursement pathways that favor cutting-edge imaging technologies. The United States, in particular, sets the pace with significant procedural throughput, extensive clinical trials, and ongoing product validation initiatives. This region’s mature ecosystem of hospital networks and outpatient centers has created diverse market segments, ranging from academic medical centers to standalone cath labs, each seeking integrated procedure room solutions.

Europe follows closely, contributing a substantial portion of the global concentration through economies such as Germany, France, and the United Kingdom, all of which are characterized by centralized procurement strategies and collaborative purchasing consortia. Here, evolving regulatory frameworks, coupled with an emphasis on hybrid operating theaters, have created distinctive market drivers that support continuous equipment upgrades. The convergence of cross-border healthcare access and multi-hospital group alliances has also influenced purchase cycles, while regional health technology assessment protocols inform investment decisions.

Asia Pacific holds a growing share of overall value, driven by rapid urbanization, infrastructure enhancements, and rising demand for minimally invasive interventions. In key countries including China, Japan, and India, expanding tertiary care capacity and government-led programs to improve vascular care delivery are shaping competitive market dynamics. Suppliers are focusing on tailored service models and flexible financing to address local needs, and upcoming initiatives in emerging economies are expected to alter the regional value landscape. Stakeholders are closely monitoring these developments in ongoing market forecast reports to align their deployment strategies with future demand patterns.

Fastest Growing Region

The Asia Pacific region is emerging as the fastest growing market for angio suites, reflecting shifting market dynamics fueled by rising procedural volumes, healthcare infrastructure expansion, and favorable demographic trends. Rapid population growth and an increasing prevalence of cardiovascular and neurovascular disorders have driven demand for minimally invasive interventional solutions, leading to notable increases in regional share vis-à-vis established markets. Multiple market drivers are at play, including government initiatives to modernize tertiary care facilities, enhanced reimbursement schemes in select countries, and public–private partnerships that facilitate capital investment in advanced imaging platforms.

In addition, the region’s evolving market segments—spanning urban tertiary hospitals, specialty clinics, and emerging ambulatory surgery centers—provide diverse entry points for suppliers, who are tailoring offerings to meet local clinical protocols and budgetary constraints. Strategic collaborations between hospitals and technology providers are accelerating the deployment of custom solutions, while regulatory authorities have introduced streamlined approval pathways to reduce time to market. These factors collectively inform market forecast models that project continued momentum through the forecast horizon, with adoption expected to outpace other regions.

As stakeholders evaluate growth strategies, they must consider varying levels of healthcare expenditures and localized purchasing criteria across countries like China, India, Japan, and Australia. By aligning product portfolios with regional priorities—such as modular imaging architectures and scalable service agreements—suppliers can capture untapped potential. Observers tracking these trends will note that Asia Pacific’s robust growth trajectory offers valuable insights into the next wave of global adoption, reinforcing its status as a pivotal growth engine in the sector.

‣ Get this Report in Japanese Language: アンジオスイーツマーケット

‣ Get this Report in Korean Language: 안지오스위트마켓

About Author:

Ravina Pandya, Content Writer, has a strong foothold in the market research industry. She specializes in writing well-researched articles from different industries, including food and beverages, information and technology, healthcare, chemical and materials, etc. (https://www.linkedin.com/in/ravina-pandya-1a3984191)