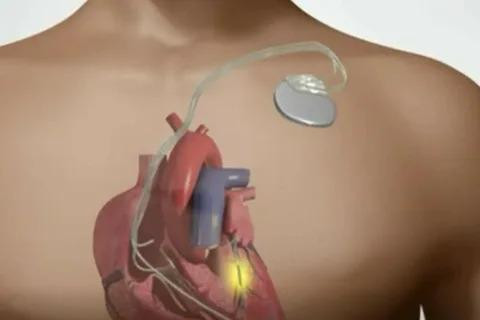

Cardiac pacemakers are implantable medical devices designed to regulate abnormal heart rhythms by delivering electrical pulses to the myocardium when the heart’s intrinsic conduction system fails to maintain optimal rates.

These devices comprise pulse generators, leads, and sensing electrodes engineered to detect bradycardia,

tachycardia, and atrioventricular block conditions. Modern pacemakers offer programmable pacing modes, rate responsiveness, and advanced diagnostics that improve patient quality of life and reduce hospitalization rates.

Advantages include minimal invasiveness, long battery life, MRI compatibility, and remote monitoring capabilities that allow clinicians to adjust therapy via telehealth platforms. Demand for Cardiac Pacemaker Market Growth is driven by increasing prevalence of cardiovascular diseases, an aging global population, and rising healthcare expenditure.

Innovative models integrating wireless communication and biometric sensors are creating new market opportunities, addressing challenges related to device miniaturization and energy efficiency.

As market players invest in research and development to expand product pipelines, competitive dynamics intensify while the latest market report highlights potential segments like dual-chamber and leadless pacemakers. With robust market drivers, evolving regulatory frameworks, and improved patient outcomes, industry stakeholders are targeting emerging markets for business growth.

Cardiac Pacemaker Market is estimated to be valued at USD 5,158.0 Mn in 2025 and is expected to reach USD 7,311.2 Mn in 2032, exhibiting a compound annual growth rate (CAGR) of 5.1% from 2025 to 2032.

Key Takeaways

Key players operating in the Cardiac Pacemaker Market are Medtronic, Boston Scientific Corporation, Abbott, BIOTRONIK SE & Co. KG, Pacetronix, and Lepu Medica. These market companies leverage strategic partnerships, mergers and acquisitions, and portfolio expansions to maintain competitive market share.

They invest in next-generation device platforms, market research, and clinical studies to address unmet clinical needs and enhance device efficacy. With continuous innovation in market dynamics, these key players are pivotal in driving market growth strategies and shaping the industry size and revenue forecasts outlined in leading market insights.

Growing demand for cardiac pacemakers is propelled by rising prevalence of arrhythmias, congestive heart failure, and bradycardia among geriatric populations. Increased awareness, improved diagnostic capabilities, and favorable reimbursement policies fuel market growth.

Market insights indicate that demand is further bolstered by technological advancements such as wireless telemetry and remote patient monitoring, which reduce hospital visits and improve long-term outcomes. Moreover, the expanding scope of indications and rising demand for minimally invasive procedures underpin market growth, presenting robust market opportunities across developed and developing regions.

Market Key Trends

A key trend reshaping the Cardiac Pacemaker Market is the surge in adoption of leadless pacemaker systems. These miniaturized, self-contained devices eliminate transvenous leads, reducing infection risks and procedural complications associated with traditional pacemakers. Leadless pacemakers offer enhanced patient comfort due to their compact size and simplified implantation via catheter-based delivery.

Advances in battery chemistry and power management extend device longevity, aligning with market drivers for improved reliability and reduced replacement rates.

Porter’s Analysis

Threat of new entrants:

High regulatory requirements and substantial R&D investments create significant barriers, deterring small firms from easily entering the cardiac pacemaker sector. Moreover, stringent clinical trial protocols and long approval timelines mean new entrants must commit substantial resources before achieving viable market share.

Bargaining power of buyers:

Large hospitals and integrated healthcare networks tend to consolidate purchasing, strengthening their negotiating position on price and service terms. These buyers demand robust clinical evidence and post-implant support, pressuring suppliers to continuously innovate and optimize device features to retain contracts.

Bargaining power of suppliers:

A limited pool of specialized component manufacturers—particularly for microelectronics and biocompatible materials—grants these suppliers moderate leverage. However, device makers often establish long-term agreements to secure steady inputs, balancing supplier power through diversification of sourcing and investment in vertical integration.

Threat of new substitutes:

Developments in leadless pacemaker technology and non-invasive cardiac rhythm management offer alternative therapies that could gradually erode demand for traditional systems. Continuous innovation in minimally invasive procedures and wireless monitoring further intensifies this substitution risk within certain patient segments.

Competitive rivalry:

Intense competition among established manufacturers and emerging innovators drives frequent product enhancements and strategic collaborations across the value chain.

Geographical Regions

North America remains the foremost region in terms of total value generation, supported by advanced healthcare infrastructure, robust reimbursement frameworks, and high procedural volumes.

Comprehensive market research underscores strong physician awareness and patient acceptance that sustain consistent device adoption. Western Europe follows closely, benefiting from established cardiology centers and collaborative clinical networks. In these territories, ongoing investments in R&D hubs and post-market surveillance programs ensure rapid integration of the latest features—strengthening regional market dynamics.

Japan and select Asia-Pacific countries also contribute sizable revenues; favorable government initiatives, expanding insurance coverage, and growing geriatric populations drive steady demand. Across these mature markets, established supply chains and specialized training facilities facilitate broad clinician engagement, reinforcing their dominant share of global revenue.

Get this report in Japanese language- 心臓ペースメーカー市場

Get this report in Korean language- 심장 박동기 시장

Read more articles related to this industry-

Active Implantable Medical Devices Market

Nanofiber Applications in Medical Devices: Revolutionizing Healthcare

About Author:

Vaagisha brings over three years of expertise as a content editor in the market research domain. Originally a creative writer, she discovered her passion for editing, combining her flair for writing with a meticulous eye for detail. Her ability to craft and refine compelling content makes her an invaluable asset in delivering polished and engaging write-ups.

(LinkedIn: https://www.linkedin.com/in/vaagisha-singh-8080b91)