Starting and growing a business requires a significant amount of capital. While there are many ways to fund a business, getting a loan can be an attractive option for many entrepreneurs. However, the loan application process can be daunting, especially if you're a first-time borrower. In this article, we'll provide a detailed guide on how to get a loan for a business.

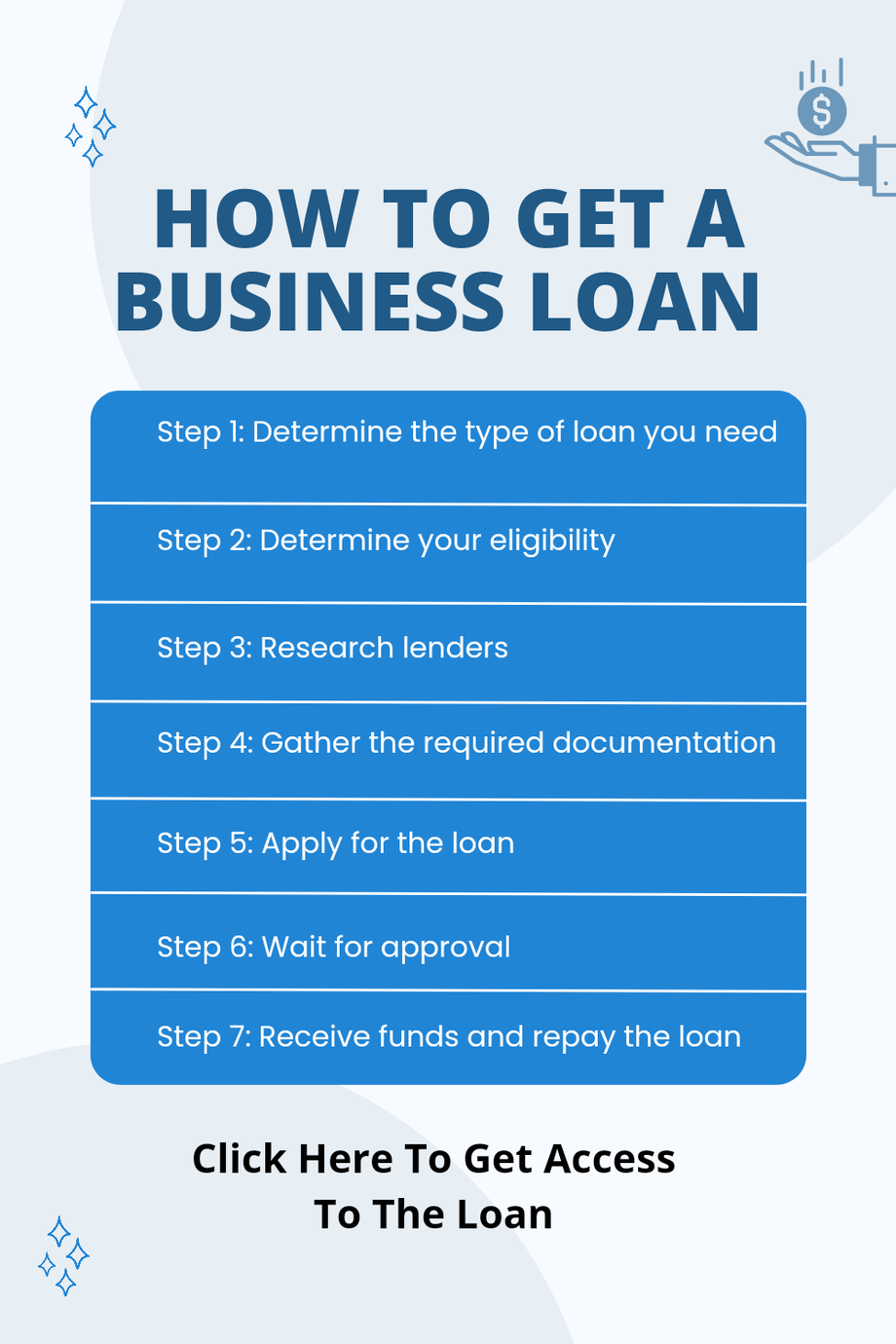

Step 1: Determine the type of loan you need

There are different types of loans available for businesses, and it's essential to determine the type of loan that best suits your needs. The most common types of loans for businesses include:

Term loans: These loans are repaid over a set period, typically between 1 and 5 years. They can be used for various purposes, including purchasing equipment, inventory, or expanding the business.

Business lines of credit: These loans provide businesses with access to funds that can be borrowed and repaid as needed. They're often used to cover short-term expenses such as payroll or inventory purchases.

SBA loans: These loans are guaranteed by the Small Business Administration and are available to businesses that meet specific criteria. They can be used for various purposes, including purchasing real estate, equipment, or working capital.

Step 2: Determine your eligibility Before applying for a loan, it's important to determine your eligibility. Lenders typically consider factors such as your credit score, business history, revenue, and cash flow when assessing your eligibility for a loan. It's essential to have a solid business plan, including financial projections, to increase your chances of being approved for a loan.

Step 3: Research lenders

Once you've determined the type of loan you need and your eligibility, it's time to research lenders. There are many lenders available, including banks, credit unions, and online lenders. It's important to compare lenders' rates, terms, and fees to find the best loan for your business.

Step 4: Gather the required documentation

To apply for a loan, you'll need to provide certain documentation, including financial statements, tax returns, and a business plan. Lenders may also require personal financial statements and collateral, such as real estate or equipment, to secure the loan.

Step 5: Apply for the loan

Once you've gathered all the required documentation, it's time to apply for the loan. The application process can vary depending on the lender, but generally, you'll need to complete an application form and provide the required documentation.

Step 6: Wait for approval

After you've applied for the loan, you'll need to wait for the lender to review your application and make a decision. The approval process can take anywhere from a few days to several weeks, depending on the lender.

Step 7: Receive funds and repay the loan

If your loan is approved, the lender will provide you with the funds, and you can use them to grow your business. It's important to make timely payments to avoid defaulting on the loan, which can harm your credit score and damage your business's reputation.

Conclusion

Getting a loan for your business can be a great way to access the capital you need to grow and expand. However, it's important to research lenders, determine your eligibility, and gather the required documentation before applying for a loan. By following these steps, you can increase your chances of being approved for a loan and take your business to the next level.